Investment Update Q2 | 2024

Roanoke Asset Management; Q2 Review and Investor Letter

Equity markets extended gains during the Q2, rising 4.2% as rising profit expectations offset broadening consensus that the Federal Reserve is likely to keep interest rates “higher for longer” than previously anticipated.

Market breadth narrowed considerably with information technology and those companies at the forefront of the AI revolution sharply outperforming. Nvdia, for example, rose 35% during the quarter and is up 156% year-to-date, accounting for fully one-third of the gain in the entire market over the same period and briefly eclipsing Microsoft, Apple, Tesla and Google to become the world’s most valuable company.

In contrast, the S&P 500 Equal Weighted Index, which averages the stock price performance of each company without regard to market capitalization, lost ground during the quarter, falling 2.4%; mega-caps are beating the broader market by more than 1100 basis points year-to-date.

On a sector basis, the dominance of technology shares was stronger than ever as evidenced by the performance table above. Technology shares rose 8.3% for the quarter while the communication services sector, which includes both Google and Meta, advanced 4.1%. The only other S&P sectors to post positive returns were consumer staples, up 1% and the utilities, which has attracted investors who anticipate growing demand for energy to power AI data centers. Healthcare, consumer discretionary, financial services, industrials, energy and materials all were down.

Style-wise, growth continues to outperform value with the S&P 500 Growth Index rising 10% during the quarter while value dropped 1%. Over the past year, growth is up over 30%, roughly twenty percentage points over value, a historically large run of relative underperformance.

Firmer inflation figures early in the quarter caused bonds to sell off with ten-year treasury yields rising to 4.7% in late April before dropping to 4.4% by the end of the period. Nevertheless, both investment grade bonds and long-term treasuries lost ground during the Q2 and are now down 2.5% and 6.6%, respectively, year-to-date.

U.S. markets continue to outperform Europe and Asia, which fell 1% and 2.5% during the quarter while modestly lagging emerging markets, which advanced 4.8%.

This outperformance has been driven, in our view, by what we believe will become a prolonged period of rising American labor productivity, aided by broad-based adoption of new technologies including artificial intelligence.

While stocks continue to power higher, earnings have kept pace. Valuation-wise, with the S&P 500Ⓡ closing the quarter at 5442, the market is trading at 21.7 times the current consensus earnings forecast of $250 for 2024 and 20.1 times the CY 2025 forecast of $270. This represents an earnings yield of 4.98% on the CY 2025 forecast versus the current 10-year treasury yield of 4.41%. The implied equity risk premium of only 57 basis points is well below the historical average, suggesting that equities are less attractive relative to bonds currently.

One offset here is the prospect of accelerating earnings growth which has historically produced solid equity market gains, notwithstanding the modest equity risk premium to bonds. The current consensus calls for nearly double digit earnings growth through the beginning of 2026, a trendline we believe will continue to support stocks in the intermediate- to long-term. Indeed, at the beginning of the year, consensus earnings for the S&P 500 were around $235 whereas the current forecast has moved to $250.

In our view, all this mandates both a research-driven active management approach as well as prudent diversification, both of which have been hallmarks of Roanoke’s strategy for the past four decades.

The Economy

The U.S. economy has proved remarkably resilient in the face of the Fed’s aggressive tightening policy. GDP growth in the Q4 was an above-trendline 3.4% and while growth moderated in the Q1 to 1.4%, over 1.0% of this decline was related to inventory adjustments, which tend to be transitory. Indeed, forecasters look for Q2 growth of 2.4% with expenditures on services offsetting modest declines in durable and non-durable goods expenditures.

We’re watching the state of the consumer carefully since personal consumption expenditures account for 68% of total economic activity in the U.S. Since the pandemic, the U.S. labor market has been extremely strong with over 30 months of sub-4% unemployment. Notwithstanding the 2021 spike in inflation, real wages have been rising since mid-2022, providing a foundation for sustained spending.

On the side of caution, the large level of excess savings buoyed by unprecedented government transfer payments related to COVID, is largely depleted with the savings rate currently hovering around 4%, down from 5.3% last year and well below the long-term average of 8.6%. At the same time, consumer debt continues to rise with credit card balances exceeding $1 trillion for the first time. Ninety-day delinquencies on credit card debt rose to 6.9%,

With a prospective softening in consumer spending, we’d expect to see moderating performance in the auto sector and among those companies selling high-ticket durables such as home appliances; yet auto sales are estimated to have risen 2.9% in the first half. While inventory levels appear to be elevated and incentives are increasing, industry experts still expect an increase in sales for the 2H with slightly lower growth pegged at 1.5% and a mix shift towards commercial versus consumer vehicles.

In the near- to intermediate-term, it’s hard for us to see a sharp pullback from the consumer. Even in the worst economy of the past 50 years, the 1974 recession, consumption declined only 2%. With wage growth strong and 96% of the population working, we anticipate a slight moderation in growth but expect the U.S. economy to track above its 1.8% growth potential through the end of 2025.

Outlook for Corporate Profits

Corporate profits remain elevated with sales and margins rising. Q1 earnings rose 7% and forecasters expect an 11% gain for the Q2. Against this backdrop, full-year estimates have trended higher with a 12% gain forecast for 2024 to $250 followed by 8% in 2025 and 11% in 2026 to $300.

The potential for AI investments to yield significant improvements in productivity is absolutely clear and could power the next leg of margin expansion in the 2026 - 2030 timeframe.

Credit Markets and Inflation

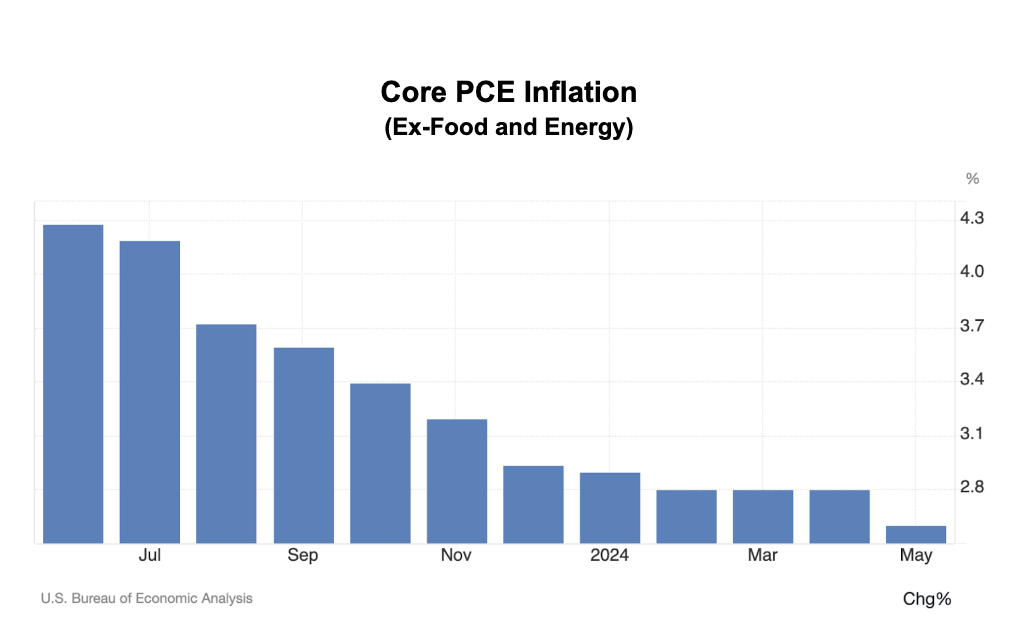

The most aggressive tightening cycle since the Volcker era has not materially dampened solid economic growth nor the strong labor market with unemployment only ticking up modestly from it’s record 2023 low of 3.4%. Inflation has moderated from its high water mark of 9.1% in June, 2022 but with recent readings hovering around 3.5-3.6%, remains stubbornly above the Fed’s 2.0% goal. Core PCE inflation, the Fed’s preferred measure, ticked below 3.0% for the first time in May, coming in at 2.6%. Should these trends continue, we’d expect to hear more talk about Fed easing in early 2025.

Market Implications

The U.S. economy is the largest in the world; labor productivity is rising at nearly a 3.0% clip, well above the 1.5% average over the past twenty years. Productivity gains have supported real wage growth, powering spending. Despite it’s size, GDP growth in 2023 was the third highest globally of the major economies. Twenty years ago, the U.S., Germany and the United Kingdom had similar levels of GDP per capital. Since then, U.S. GDP per capita has nearly doubled while Germany and the U.K. are up 42% and 14% respectively.

We see this relative outperformance continuing and potentially accelerating given a number of factors including the importance we attach to new applications of artificial intelligence and machine learning, companies leading this revolution are mostly U.S.-based. Assuming the U.S. does not adopt draconian policies around immigration - a key support of productivity and economic growth - we also expect the U.S. to avoid the demographic spiral now gripping several members of the European Union.

Given this backdrop and the prospect of well above trendline earnings growth expected over the next 18-24 months, we remain constructive on equities. We do expect temporary pullbacks in the high-flyers where momentum investors are driving stock prices but even in the case of a company like Nvidia, this is a business that is generating annualized free cash flow approximating $40B, growing over 100% in recent quarters. And while the overall market is expensive, underneath the covers there are ample attractive opportunities to identify well-managed companies at reasonable prices - ex-NVDA and the top 7 mega-cap names, the market is trading a more reasonable 16 times forward earnings.

This market environment makes passive investment strategies particularly imprudent. Roanoke’s style of appropriate diversification, tax-aware portfolio construction and a long-term investment orientation provides important ballast to windward in uncertain times. Our ability to identify winning business models over the long-haul, irrespective of macro considerations, which are currently very much in flux, is particularly impactful today.

As always, if we can clarify or elaborate upon our current thinking, please be in touch. We like hearing from you.